Before you buy a house in London, establish a clear buying framework and run through essential checks: confirm age, extensions, and legal status from property records; inspect the roof, foundation, damp, and signs of structural repair; assess proximity to transport, amenities, and crime or safety metrics that affect demand; compare recent sales to gauge fair value; verify planning permissions and zoning; and consider ongoing costs, legal issues, and future renovation potential. Do these steps now to uncover potential pitfalls and open a confident decision.

Establish Your London Buying Framework

Establishing your London buying framework starts with a clear plan that aligns your finances, timeline, and priorities. You map your budget, including upfront costs, stamp duty, and ongoing charges, to a realistic housing target.

Define non-negotiables, such as preferred boroughs, commute tolerance, and lifestyle needs, then translate them into measurable criteria.

Assess property zoning implications for potential additions or alterations, ensuring you understand restrictions that affect future plans.

Consider neighborhood safety metrics, crime trends, and access to essential amenities, weighing them against your desired pace of purchase.

Build a decision matrix that ties each criterion to a milestone date, so you can track progress and adjust as market conditions shift.

Document your framework, review it quarterly, and align it with loan capacity and risk tolerance.

Inspect London Property Age, Structure, and Repairs

When inspecting a London property, you should assess age, structure, and repairs with a methodical, evidence-based approach. Start with records: building age, prior extensions, and any listed status.

Check the roof, walls, foundation, damp, and timber for signs of wear or past remediation. Look for inconsistent plaster, cracks, or moisture that signal structural issues or hidden repairs.

Verify services—plumbing, electrical, heating—and ascertain compliance certificates.

Assess roof integrity and drainage, ensuring gutters channel water away from the building.

Consider renovation costs by factoring in potential upgrades, insulation, and wiring updates in line with current standards.

Document findings for a professional valuation, and include contingencies for unexpected repairs.

Use the data to determine total property valuation and funding needs before making an offer.

How Transport, Amenities, and London Neighbourhoods Impact Price

Transport links, local amenities, and the character of London neighbourhoods measurably shape property prices by influencing daily convenience, potential rental income, and long-term capital appreciation. You assess proximity to major transportation hubs, including rail and Underground stations, to gauge time savings and demand from commuters.

Reliable bus routes, cycle lanes, and walkability boost appeal for families and professionals, supporting higher offers in progressing markets.

Local amenities—parks, schools, supermarkets, cultural venues—create sustained demand beyond cosmetic appeal, aiding price stability even in downturns.

Luxury neighborhoods often command premium due to curated streetscapes and perceived safety, while proximity to frequent transport hubs can shorten vacancy cycles for investors.

Weigh the balanced mix of transport access and neighbourhood vitality to estimate resilient resale value in varied market conditions.

Read Price Signals and Market Trends Before Bidding

To bid effectively, you should read price signals and market trends before making an offer. You’ll examine current market valuation to gauge whether prices are rising, stabilizing, or declining.

Track price fluctuations over recent weeks and months, noting how swiftly values move after market updates, seasonal shifts, or policy changes.

Compare listings in similar London districts to assess relative strength or weakness in demand. Consider volume of sales, time on market, and how quickly properties attract offers.

Factor in macro influences like interest rates and lender appetite, but prioritize the data you see locally.

Use these signals to set a realistic ceiling, avoid chasing peaks, and time your bid to align with genuine buyer activity rather than rumors.

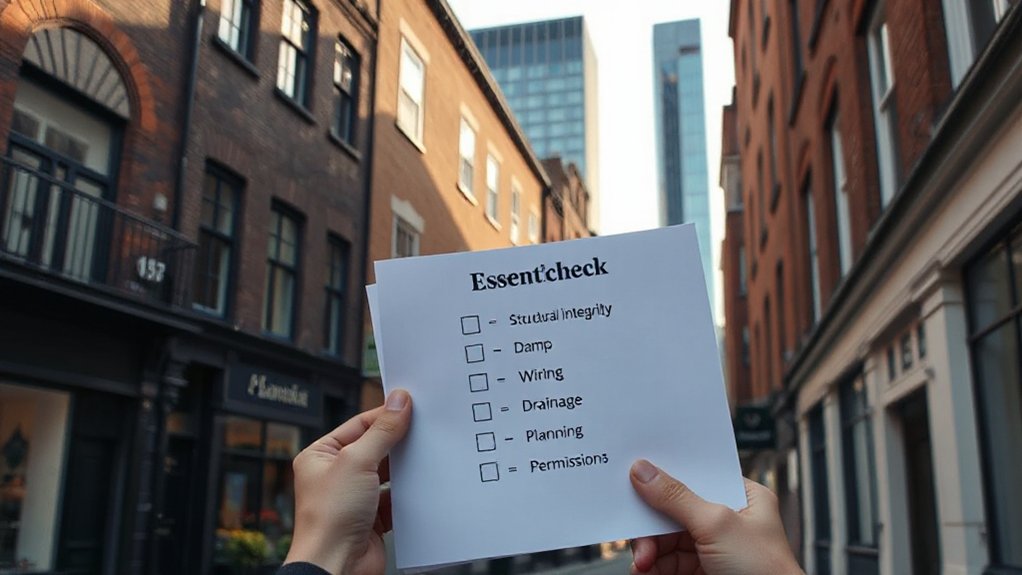

A Step-by-Step Due Diligence Checklist to Avoid Overpaying

A step-by-step due diligence checklist helps you avoid overpaying by systematically verifying every major facet of a property and its market context before you bid. You assess recent comparable sales, rental yields, and time-on-market to gauge fair value, then corroborate with formal records.

Next, review legal considerations, including chain encumbrances, title defects, and any restrictive covenants that could influence use or resale.

Inspect the property for structural integrity, damp, and required repairs, documenting findings with photos and notes.

Confirm property tax history, current rates, and any impending changes that affect affordability.

Verify planning permissions and zoning to prevent surprises after purchase.

Finally, align your bid with the verified price, risk, and your budget, and set a clear stop-loss.

Frequently Asked Questions

How Do Lease Terms Affect Long-Term Costs in London?

Lease duration affects your long-term costs: longer terms mean lower annual ground rent initially, but you may face higher renewal or negotiation fees. You’ll likely pay for ground rent increases or caps; track terms, timing, and potential protections carefully.

What Hidden Costs Come With Buying in Central vs. Fringe Areas?

Like a careful compass, you’ll weigh hidden fees and market trends as you compare central vs. fringe areas. You’ll uncover hidden fees, study market trends, and assess ongoing costs to make a thorough, objective, informed decision.

Are School Catchment Areas Negotiable in Property Pricing?

Yes, school zoning and catchment boundaries can influence price, but not usually renegotiated directly; you negotiate overall value, then leverage favorable catchment proximity and stability as part of your offer, considering zoning maps and boundary changes.

How Does Flood Risk Influence Insurance and Resale Value?

Flood risk assessment shapes your insurance implications: higher flood risk can raise premiums, restrict coverage, or require mitigation. You should obtain official flood risk data, inspect property measures, and factor resale value changes into your decision.

What Are Common Title and Boundary Issues in London Homes?

Title deeds reveal hidden maps; boundary disputes loom like shifting hedges. You check boundaries, encroachments, and historic rights, documenting every line. You examine title deeds carefully, confront ambiguities, and preserve your claim through precise, methodical records.

Conclusion

You’ve done your homework, mapped the terrain, and armed yourself with numbers. Now, breathe in the clarity: your due diligence is a steady compass guiding you through price signals, permits, and potential repairs. With every checklist item checked, you reduce risk and sharpen your negotiating edge. Like a seasoned navigator, you’ll chart a course through transport links, local vibes, and hidden costs, landing on a solid value and a home that fits your London story.